Iran War: Oil Prices Jump as Markets Weigh the Risks

The fragile peace between the United States and Iran was shattered at the end of February when the US and Israel launched an attack on key Iranian military targets and the nation’s leadership.

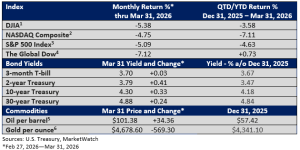

Thus far, the market’s response has been relatively restrained. Since hostilities began, the S&P 500 has shed a modest 5.09% from the pre-war February 27th level to the month’s end. The peak-to-trough decline: 9% (St. Louis Federal Reserve data on the S&P 500).

By comparison, the S&P 500 dropped just over 10% in the two days following last April’s Liberation Day tariff announcement.

This modest pullback occurred despite Iran’s closure of the Strait of Hormuz, a key global energy chokepoint that accounts for about one-fifth of global oil flows—about 20 million barrels each day, according to the Energy Information Administration (EIA).

Some of the disruption has been made up by releases from global strategic petroleum reserves, workaround pipelines in the Persian Gulf, and an increase in output from non-OPEC nations.

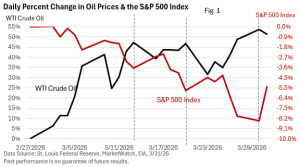

Even so, the shock has been jarring for the global oil market, triggering sharp price swings and putting pressure on equities, as highlighted in Figure 1.

While the sudden rise in price has created pain at the gas pump, Figure 2 shows that inflation-adjusted prices are not unprecedented by historical standards.

Beyond oil, disruptions to helium—essential to semiconductor production—fertilizer, and aluminum exports from the region are raising the risk of supply chain strains and higher costs if the Strait remains blocked for an extended period.

Key asset reaction—four asset classes

1. The US dollar has resumed its status as a safe haven for foreign cash. Fading expectations of a rate cut have also lifted the dollar.

2. Equities declined in March, but losses were limited by expectations that the war would be brief. A resilient economy and solid corporate earnings also helped cushion the downside.

3. Treasury yields have risen amid worries about an uptick in inflation. Historically, bond yields decline during a crisis, as investors seek safety in Treasury bonds (bond prices and yields move in opposite directions). According to Bloomberg, some Middle Eastern nations may have reduced their holdings of US Treasuries amid a need for cash.

4. Finally, precious metals, which have historically been a refuge in times of uncertainty, came under heavy pressure.

Gold also faced headwinds from rising bond yields, which reduced its appeal as a non‑yielding asset. Global central bank sales may have added to the pressure, per Bloomberg.

Final thoughts

Despite economic headwinds tied to rising oil prices, the overall market decline remained relatively contained.

Expectations that the conflict would be limited in duration helped stabilize sentiment, while a resilient US economy and generally solid corporate earnings provided support.

Investors also took comfort in the perception that the Federal Reserve was unlikely to overreact to a supply-driven rise in oil prices.

As a result, March was marked by higher volatility yet modest losses rather than panic-driven selling, leaving markets cautious but still fundamentally supported heading into April.